Methodology Paper

Impact investments have come into their own as an investment approach in recent years. Projections for growth vary, but despite uncertainties around the actual volume of such investments, and how they are defined, demand is increasing. At Zurich Insurance Group (Zurich), we define impact investing as investment opportunities that allow us to intentionally target a specific social or environmental impact, provide a measurable impact, and generate a financial return commensurate with their risk. We as an insurer serve an important role in society, providing protection and helping companies and individuals to protect against risk. By extension, we believe that impact investments have the potential to drive positive changes.

To achieve that, having clear processes and guidelines in place to calculate the impact that defines this investment approach is essential. Our experiences in this regard may also serve as guidance for others who have engaged in similar journeys. We believe that sharing how we have set out to calculate the real impact of these investments could also lead others to measure their impact and link their investments to positive outcomes.

Zurich Insurance Group as an impact investor

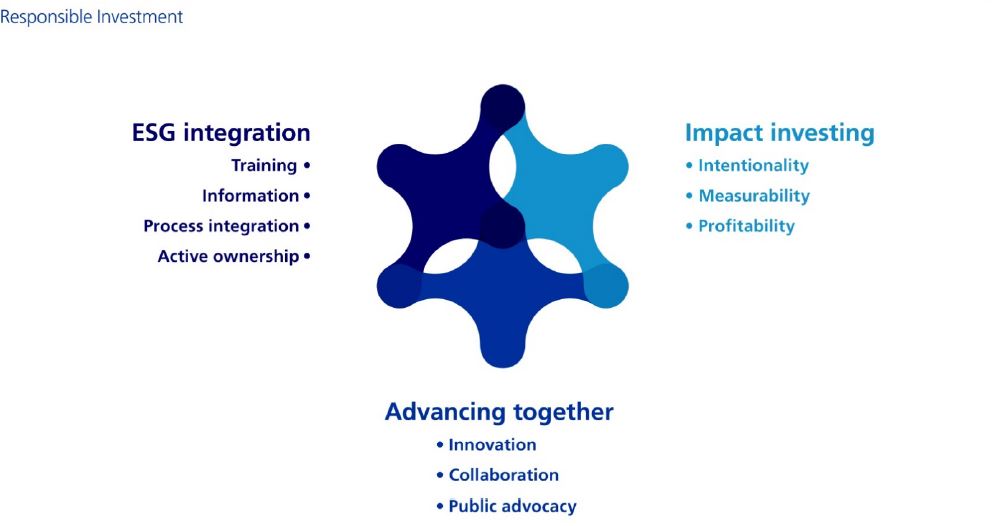

Responsible investment forms a key element of Zurich's investment philosophy and comprises three elements:

- ESG-integration: Proactively integrating environmental, social and governance (ESG) factors in the investment process – across asset classes and alongside traditional financial metrics and state-of-the-art risk management practices.

- Impact investing: Through impact investing, Zurich can help fund solutions to pressing social or environmental issues.

- Advancing together: We believe that responsible investment will only truly have an impact if financial market participants’ advance together to make responsible investment a mainstream approach.

As an insurer, we have a direct interest in promoting sustainable global economic growth and supporting communities in becoming more resilient to environmental and social challenges. Impact investments can help address these issues in a targeted way, and also offer a financial return commensurate with risks. We define impact investing as investment opportunities that allow us to intentionally target a specific positive social or environmental impact and allow us to measure the impact achieved; these are profitable, meaning that they generate a financial return commensurate with their risk.

Through our impact investments we target positive outcomes in two main ways:

- Mitigating environmental risks by supporting a low-carbon economy and encouraging environmentally-friendly technologies, measured in terms of ‘reduced/avoided CO2 emissions.’

- Increasing community resilience by helping to build ‘community capital,’ and addressing the needs of populations that lack traditional means to achieve such goals (the ‘under-served populations’), measured in terms of ‘the number of people who benefited.’

We acknowledge that for an investment to be counted as an ‘impact investment,’ it is the inherent impact that an investment can achieve that we must consider. It is important to ‘measure what matters’ using various impact metrics, based on how relevant or applicable they are for various types of investments.

However, for our purposes we focus on two metrics – ‘CO2 emissions avoided’ and ‘people benefited’ – as we see these numbers being regularly collected and reported by market participants, and these metrics are relevant for different project categories, making them available to be added across asset classes and instruments.

As an impact investor, Zurich is committed to investing up to USD 5 billion in impact investments. At this level, we aim to avoid five million tons of CO2 equivalent emissions per year, and, separately, believe we can make a positive contribution to the lives and livelihoods of five million people.

1.1. Scope of impact portfolio

Zurich evaluates impact investments within the context of specific asset classes and creates dedicated strategies for impact investment within each of those asset classes. While continuing to make systematic use of environmental, social and governance (ESG) data in investment decision-making, we look at a variety of ways to grow our impact investment portfolios around the world. We focus on the following asset classes:

• Fixed income: use-of-proceed bonds encompassing green, social, and sustainability bonds.

• Impact private equity: We will keep working toward achieving our 10 percent impact target in private equity based on our overall private equity portfolio.

• Impact infrastructure private debt, including direct private debt lending toward infrastructure such as solar/wind farms and social institutions.

• Real estate: Our Swiss real estate portfolio, which is our largest real estate portfolio, has emission reduction targets.

1.2. Why we measure

Besides tracking our exposure and targeted returns, we want to know what each of our investments achieves in terms of impact, and measure our contribution toward our impact investment objectives: mitigating environmental risks and increasing community resilience. Measurement helps us make better investment decisions and allows us to communicate our value to our shareholders. It also demonstrates that financial returns can be balanced with environmental and social returns. As the first private-sector investor to commit to specific impact targets, which Zurich did in 2017, we deliberately chose to challenge ourselves to develop a methodology that allows us to measure impact on portfolio level – across asset classes and underlying investment instruments.

Together with BlackRock we developed a standardized approach to aggregate use-of-proceed impact data across various bond issuers along the metrics of ‘CO2 emissions avoided’ and ‘people benefited,’ ensuring we only account for the impact we effectively finance.

First step: gathering reported impact numbers

Zurich’s impact measurement methodology is based on impact data reported by the issuers of impact investing instruments.

The issuer or manager is the closest to the project and best placed to have actual raw data or best positioned to make reasonable and adequate assumptions – far better placed than we as an investor not involved in the actual project. While we acknowledge the short-comings of self-reported data, i.e., heterogeneity of assumptions, different base-line assumptions and methodology, we believe this is a better approach than trying to calculate that data ourselves or with the help of external consultants.

2.1 Definition of metrics

As stated, while we do take into account various impact metrics suited to specifications of different impact investments, we focus on two metrics, believing these are the most commonly used, which provide us with an opportunity to aggregate them.

2.1.1. CO2-equivalent emissions

Zurich’s impact investment objective ‘mitigating environmental risk’ is measured in terms of reduced/avoided greenhouse gas emissions.

Data on emissions of greenhouse gases (generally quoted in tons of CO2-equivalent emissions) is a commonly used indicator to assess the climate impact of an asset as established by the IFI harmonized framework.

‘Avoided’ CO2 emissions are calculated against a baseline scenario that reflects the most likely project outcomes or level of service achieved in the higher-carbon status quo of the economy (also referred to as ‘net’ or ‘relative’ emissions; subtracting the baseline emissions from the absolute, or gross emissions, equals the emissions ‘reduced/avoided’).

2.1.2. People benefited

To measure our social objective to ‘increase community resilience,’ we count the number of people who have benefited from services in education, health, housing, or financial inclusion and other measures aimed at improving lives, improvements that are directly related to Zurich’s investments. Unlike to ‘CO2 emissions avoided,’ there is no common market definition for ‘people benefited.’ While the metric is commonly reported, looking into the reported details is important, and it is necessary to set one’s own standard.

In our measure of ‘number of people who benefited,’ we only count those individuals who are part of a specific targeted audience that previously was unable to access those services. We seek the definition for the target audience reported in the impact report. By and large we would look at an audience that benefits from services in education, health, housing or financial inclusion, but other target groups could also be considered.

Zurich aims to measure the actual number of people benefited, as opposed to the potential audience, the latter called ’catchment.’ However, we realize that for some projects, the real number of beneficiaries might be difficult to capture, e.g., a bicycle path that can be used by the population of an entire city. Where only ‘catchment’ numbers are provided, we make this clear in the footnotes of our impact report.

Zurich measures the number of individuals benefiting from a service and/or product. As the term ‘benefiting’ suggests, the service and/or product need not be directly related to the individual(s) who benefit.

We take a more cautious approach for education and health, where we only take the direct link from service/product to the people who have directly benefited. However, validated academic research leads one to conclude that by providing a micro loan to an individual improves not only the quality of life for that individual, but also for their families, hence we propose to take household size as a multiplier for financial inclusion. In cases where household sizes are indicated, e.g., often being the case in energy or housing, we also use the national household multiplier.

The following multipliers are applied:

Health: 1 hospital bed = 1 individual benefited

Education: 1 pupil/desk = 1 individual benefited

Financial inclusion: 1 customer = national household size

Social housing: 1 flat = national household size

Energy: 1 household = national household size

Community: 2 individuals

Households: national household multiplier

2.2. Standardizing impact numbers

We are aware that, by using self-reported numbers and measuring impact through two rather broad impact metrics, we are summing up a heterogeneous field of impact numbers (‘adding up apples and pears’). By applying a strict definition of what an impact investment is and looking into the wider set of impact metrics for specific investments, we can be fairly sure that the quality of our impact investments is upheld.

However, to aggregate across portfolios and asset classes, a certain standardization is necessary. We have identified two areas we believe are of special importance: annualization and pro-rata shares.

2.2.1 Annualization

Zurich wants to be able to match an investment’s impact to a portfolio’s invested amount over a series of years. We thus seek to provide impact numbers on an annualized basis, rather than calculating the impact over the entire life of the project, or over the financing period. It is in our own best interest to report only the impact of what we effectively finance. While we hold most impact investments to maturity, we also may trade some of our investments. As we report on an annual basis, reporting the impact at a specific cut-off date seems appropriate (for us, the date is December 31).

While we acknowledge that the marginal impact of an underlying asset might change as the asset matures (e.g., decreasing impact with changing base-line numbers), the average – hence annualized – impact data over an asset life-cycle will provide a balance of the ramp-up and the full operation period.

2.2.2 Pro-rata/avoiding double counting

To make sure we count only the impact an impact investor is financing, impact investors are encouraged to report pro-rata shares. If an impact investor claims the full positive impact of every project, the impact investor would overstate his or her achievement.

Fixed-income: For use-of-proceed bond issuers, the pro-rata share is calculated as the impact based on the share of the total project cost that is eligible for the specific use-of-proceed bond.

• Sum of pro-rata impact of issuer = Total project impact × % Share of total project financing × % Eligibility for use-of-proceed bond (a1)

Private equity: The pro-rata share is based on the fund’s ownership structure within the relevant portfolio company

• Pro-rata impact of private equity funds = Total portfolio company impact × % Fund ownership in portfolio company (a2).

Impact infrastructure private debt is described below (a3).

2.3. Reporting structures

Depending on how proceeds are allocated, there may be differences in the impact reporting approach.

2.3.2 Allocations to a portfolio of projects (project pool)

This approach is often seen in impact reports of supranational organizations, as they often have a specific pool of their own projects.

Allocated currency (‘CCY’) amount:

• Summarized outstanding CCY up to and including the date referred to in the impact report (excluding matured issuances) (b1.1) e.g., the ‘March 2018 issued impact report refers’ to an impact achieved in 2017, includes outstanding issuance up to and including December 31, 2017. Summarized outstanding CCY is relevant, given that not only the most recently issued bond, but also the invested capital in the project ‘pool,’ contributed to the full reported impact.

2.3.1 Allocations to individual projects

Project-by-project report vs. portfolio report based on portfolio allocations.

• Project-by-project report: Identifies the specific projects and clearly defines, for each project, the total results of the project (including financing from all financiers), providing information about the total project size and/or the issuer's share of total financing.

– If the impact numbers are reported by project, the pro-rata impact numbers a1) need to be consolidated.

• Portfolio report: Aggregates project-by-project results, but includes only the pro-rated share (as a percentage of the issuer's share of the total financing) of total results of projects.

Applicable for:

• Use-of-proceed issuers – mainly corporate issuers – that allocate their proceeds to specific projects, reported per International Securities Identification Number (ISIN).

• Private equity funds, when projects refer to portfolio companies. Preferably the fund reports company-by-company.

Allocated CCY amount:

• Use-of-proceed issuers: outstanding CCY of those bonds where impact is reported (per ISIN) (b1.2), taking the sum of all outstanding CCY if the issuer has several bonds outstanding with respective reported impact.

• Private equity funds: Fund capital raised (b2).

The outstanding CCY or fund capital raised is relevant when it comes to matching the underlying projects for which the issuer/manager reports the impact as this amount will be taken as the dominator in the calculation for the pro-rata piece that is Zurich’s share. Please see the next step for more detail.

Second step: aggregating on portfolio level, across asset classes

Zurich’s impact framework methodology looks only at the impact created by Zurich’s share of investments, and it is based on the information reported by the issuers of the various impact investing instruments, as stated under the first step.

3.1. Fixed income

- For use-of-proceed bond the pro-rata share is based on Zurich’s outstanding issuance toward the specific investor. Depended whether the issuer uses the allocation to a portfolio of project or to individual projects this approach varies slightly:

- Allocations to a portfolio of projects: (x) Impact pro-rata for Zurich’s share = Full impact of the project pool (a1) × (Zurich outstanding issuance toward specific issuer / full outstanding CCY as of time impact report refers to (b1.1)); or

- Allocations to individual projects: (x) Impact pro-rata for Zurich’s share = Full impact of the issuance (a1) × (Zurich outstanding issuance toward specific issuer / outstanding CCY of issuance (b1.2)) – in case in case the issuer has several bonds issued – with respective impact reported, reported impact (a1) and outstanding CCY (b1.2) should be the sum of all issued and reported bonds, reflecting an average impact number this issuer is able to achieve.

- Summarize (x) for all use-of-proceed issuer in the portfolio (y1).

3.2. Private equity

In private equity, Zurich’s pro-rata share is based on committed capital as percentage of total fund capital raised as of a specific date.

- (x) Impact pro-rata for Zurich’s share in specific PE fund = Total impact fund pro-rata share (a2) × (Zurich committed amount / Fund capital raised (b2)).

- Summarize (x) across full Private equity portfolio (y2).

In line with the concept of ‘counting the impact for your outstanding amount with an issuer,’ we count the impact in private equity investments for the portion of committed capital, knowing that the full committed capital will not be invested from the start of the investment period. This could potentially increase the reported impact, if and when the fund buys into additional companies based on the same amount of committed capital, given that an increasing amount of the total capital will be deployed.

A note of caution: ignoring the debt portion of the portfolio company’s financing could lead an equity investor to overstate the impact of investments. Through dialogue with fund managers, we see a pro-rata share method, as proposed, as representing a start to further refinements in overall accountability.

3.3. Infrastructure private debt

Providing debt to an investments does not necessary provide you with access to the full information required to calculate the pro-rata share, i.e. equity portion invested, hence a few assumptions are required. The assumption for the capital stack is based on conversations we had with asset managers active in the sector.

Proposed pro-rata share structure:

- Assumption on capital stack: 20% equity / 80% debt for infrastructure deals

- (x) Impact pro-rata for Zurich’s share = Full impact of the project/fund/ issuance (a3) × 80% (Debt portion in capital stack) × (Zurich’s share of debt/ full project debt)

- Summarize (x) across full infrastructure portfolio (y3)

3.4. Real estate

While contributing to the overall company goal of avoiding 5 million tons of CO2 emissions, Swiss real estate has also its own specific impact targets. We measure the carbon emissions (CO2-equivalent emissions) released on an annual basis, in order to track the decrease. The carbon emissions calculation is based on the definition of ‘Ökobilanzdaten im Baubereich/eco-bau.’ This is based on a life-cycle approach and contains emissions scope 1, scope 2 and scope 3 of the claimed energy systems. The carbon emissions stem from use of electricity and heating, calculated based on the greenhouse gas emission coefficients from the collected energy consumption values. The data is climate-adjusted, meaning taking out the influence of differently cold winters.

• Annual CO2 emission avoided for full portfolio = difference of CO2 emission released from FY 0 compared to FY -1 for the full portfolio (y4)

As we fully own our real estate un-leveraged, no pro-rata adjustment is required.

Once we have calculated Zurich’s impact share per asset classes, we summarize all impact numbers for Zurich’s financed share (y1) + (y2) + (y3) + (y4) to get to impact pro-rata for our full impact portfolio.

Timing

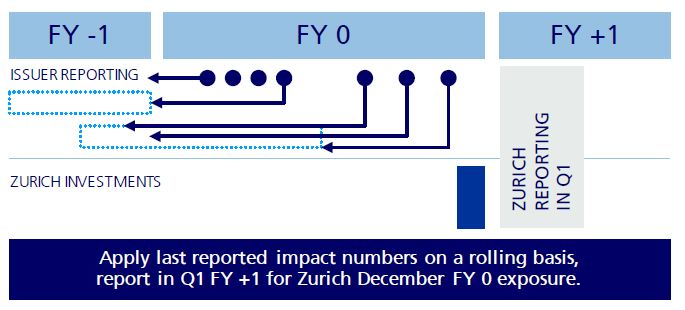

Zurich aggregates the impact numbers on a rolling basis. Impact reports are published by issuers of impact investing instruments throughout the year, depending on their own financial-year end, when they typically report impact.

Zurich reports its impact in the first quarter of the full year (Q1 FY) +1 for its financial year end 0 (FY 0). The impact refers to the following underlying invested amounts for:

Fixed income:

• Based on outstanding amount to an issuer as per end of December FY 0.

– This way of accounting allows us to implicitly extrapolate an issuer’s impact that was reported for FY -1 by the amount of additional bonds we bought later in the year (during FY 0).

– For issuers with a ‘portfolio of projects (project pool) ‘allocation approach, this will make no difference, as the impact reported will be approximately the same for FY 0 and FY -1 given the same pool of projects in FY 0 and FY -1.

– For issuers with an ‘individual project’ allocation approach in cases where the issuer has several bonds issued: With respective impact reported, reported impact (a1) and outstanding CCY (b1.2) should be the sum of all issued and reported bonds, reflecting the average impact this issuer was able to achieve.

Impact private equity:

• Based on committed amount as of FY 0.

– FY 0 will be the same as of FY -1, except in the rare cases where we might have bought into the fund on the secondary market or added exposure via a secondary market transaction.

Impact infrastructure private debt:

• Based on exposure as per end of December FY 0.

Real estate:

• Based on provided impact data as per end of December FY -1.

Limitations

By no means do we believe this is the ‘one and only’ approach to calculating the impact of a multi-asset portfolio.

While we believe the proposed methodology can be seen as a start, we are aware of the limitations it has, such as the following shortcomings:

• Various baselines and other assumptions.

– Given we are reporting based on self-reported data by issuers, we disregard – at this stage – different baselines and methodologies when reporting on aggregated CO2 emissions avoided.

– We recognize it’s a shortcoming, but believe this is the best we can use currently by relying on self-reported publicly available information from the issuers.

– Applying the IFI harmonized framework sheds light on the assumptions issuers/impact investors have used and ensures a certain alignment in methodology, applicable one-to-one for use-of-proceed bonds. It can also be used to guide impact investors in other asset classes, i.e., the pro-rata approach in private equity fund reports.

• Discrepancy in timing of impact reported versus the underlying exposure to the investment.

– Impact reports of issuers may lag by up to one year after date of issue, hence the impact data of the most recent issues is not included when Zurich calculates its latest level of investments.

– The implicit extrapolation, described above under timing, is taking account of that.

– This approach thus very likely underestimates the actual impact, as additional projects have been added during the period in question, and a higher impact might have been achieved from ‘learning by doing.’

Conclusion

Within the limitations we are aware of – and more to be found out – we see this framework as a start for further development.

While we hope others will benefit from our experience and also measure their impact and link their investments to positive outcomes, we are interested to learn from their experiences and share ideas for improvements.

While the methodology presented here aims to take a pragmatic approach without losing important details, it is admittedly a very labor-intensive process. The first hurdle to overcome was sometimes just finding the issuer’s reported impact, as this might be included in a sustainability report, an investor presentation or within a specific impact report.

We do have a few ideas on how to make this approach easier, and we also welcome any recommendations from others on how we might improve and strengthen the methodology set out here.

And the investment community can also contribute to making things easier:

- Provide your impact reports where they can be readily found! The information and details provided are very relevant.

- Report according to the IFI harmonized framework and be as transparent as possible.

- We need to work together to develop a framework for the social metric ‘people benefited.’

- If you report on project level, please report the sums of your impact data and/or provide the excel sheets.

Click here to download the full report for appendix and illustrative example.

Peter Teuscher is a member of II Network. To discuss the content of this article and further engage with him, comment below or Sign up today.