Creating a framework to target, manage and measure the social and environmental impact of our investments

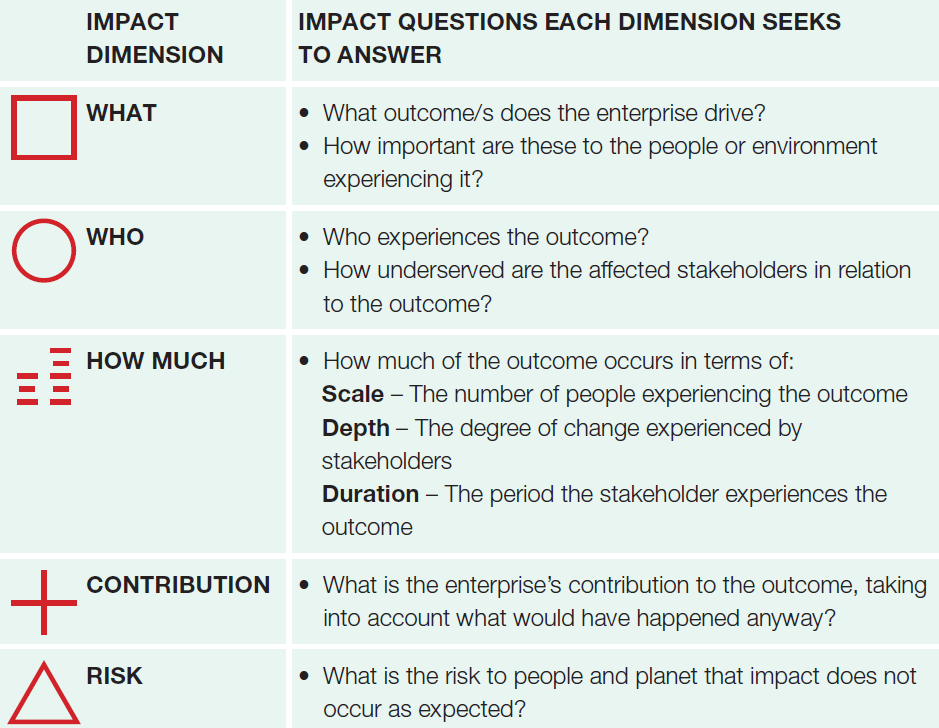

Aaron Pinnock, Impact Investment Analyst at Church Commissioners for England shares his white paper where he deconstructs investment impact in terms of its primary activity; the beneficiaries it is serving; the scale, depth and duration of the activity being delivered; its contribution to positive outcomes that would not have happened anyway; and the risk of impact not happening as expected. You can access the full report by downloading it here.

Introduction: Taking our first steps into impact

The Church Commissioners for England manage an £8.7bn investment portfolio. Our aim is to generate a total annualised return of inflation (CPIH) + 4% over the long term in a responsible and ethical way. We use the returns we generate to support the mission of the Church of England, including grants for mission activities, bishops and cathedrals.

UN SDGs driving institutional interest in impact

The topic of how to invest capital so it can have a positive social or environmental impact in the wider world – while also generating an above-inflation return to support our core mission – is of growing interest to us, as it is to many other institutional investors.

The 2016 Paris Agreement on Climate and the launch of the United Nations’ Sustainable Development Goals (SDGs) in 2015 have particularly inspired a wide range of institutions to look at how their activities can explictly benefit people and the planet. But the issues of which impacts to target, how to achieve and manage those targets and – most important of all – how to measure and manage the actual outcomes achieved are still at a very early stage of development.

This paper shares our approach to our first impact measurement exercise across our total portfolio, from the implementation of a framework through to our experience of assessing a multi-asset portfolio for impact alignment. We highlight what we have learnt from this process and the next steps we intend to take.We have written this paper to share our own thoughts and lessons learned, as well to help develop this evolving area of responsible investment by encouraging debate and learning from others. We are very keen to hear feedback from all stakeholders. Please send any feedback to Aaron Pinnock at aaron.pinnock@churchofengland.org

Why we are looking at impact investment and assessment

Like many other investors, the Church Commissioners believe that incorporation of responsible investment practices such as environmental, social and governance (ESG) integration, action on climate change, and shareholder engagement and voting can enhance investment returns. As such, these practices are consistent with our fiduciary duties, and as an asset owner, they have long formed part of our investment process, and that of our investment managers.

We knew that many investments within our portfolio were creating positive outcomes for society. But we also knew that there were areas across our portfolio where we needed more information.

Expectations Of The Investor’s Role Are Shifting

In recent years, expectations of many investors among their beneficiaries and broader society have evolved, shifting from ‘doing no harm’ to ‘doing good’. This is certainly true as a faith-based investor, but it is no less true for pension funds whose future retirees overwhelmingly support a transition to a more sustainable and fairer world.1 Industry guidance from bodies such as the UN’s Principles for Responsible Investment (PRI), and regulation such as the UK’s new Stewardship Code, have also put an increasing focus on investing for positive outcomes.

The Fiduciary Case For Impact Is Growing

Underpinning this focus is the fact that the fiduciary case for impact investing is becoming clearer. Climate change, for example, is a systemic issue that – left unaddressed – will have a significant negative effect on long-term investment returns. Portfolios are most likely to perform best in a world that limits climate change. In turn, portfolios positioned for the transition to a low-carbon global economy are likely to perform better than those that are not.

The increasing number of investors committing to net zero carbon emissions targets – either through groups such as the UN-convened Net Zero Asset Owner Alliance, or through internal commitments – demonstrates not only the importance of this transition, but the role that investors can and should play in moving to a more sustainable world.

Effective Outcomes Require Going Beyond ESG

The challenge now for investors is how to enhance positive real-world outcomes, while delivering investment returns consistent with their fiduciary responsibilities in both the short and long term. The consideration of environmental, social and governance (ESG) factors goes some way to address these concerns. But the primary focus of ESG is as a tool for investors to assess a company’s internal operations to manage these types of risk, rather than looking at the broader outcomes of investment activities. An additional focus on investment outcomes, therefore, can help investors direct capital towards better outcomes for society, which in turn address the systemic issues that we face.

Creating A Portfolio-wide Approach To Impact

Against this background, the Church Commissioners looked to formalize our approach to enhancing the positive environmental and social impacts that could be generated by our portfolio. Anecdotally, we knew that many investments within our portfolio, as well as our actions as investors, were creating positive outcomes for society. But we also knew that there were areas across our portfolio where we needed more information to help us better understand both the positive and negative outcomes being generated by our holdings.

We therefore wanted to establish an approach across our whole portfolio that would help us systematically improve the real-world outcomes of our investments. On the following pages, we outline the steps we’ve taken to determine what that approach should be.

First, we outline how we created our impact framework. We focus on how we defined the core requirements for our impact approach and how we agreed our impact priorities, before addressing the method we developed to measure our real-world impact, building on the Impact Management Project’s five dimensions of impact.

We then discuss how we assessed our portfolio against this framework, before outlining the key things we learnt about both our portfolio and the process.

Finally, we note the next steps we plan to take and reflect on what we have learnt from this process. We were struck by the fact that while impact is a new way of looking at our portfolio, it is a complement to our existing responsible investment practices that will not only deliver on our beneficiaries’ and our own non-financial goals, but is also consistent and additive to our fiduciary responsibilities.

Creating our impact framework

The process of creating a framework to target, manage and measure impact across our whole investment portfolio began in early 2019. Taking the time to consult with stakeholders, peers and industry bodies and to draw on the best of existing practice has enabled us to establish an initial approach that continues to evolve.

STEP ONE: DEFINING AN APPROACH THAT WORKS FOR US

The first step we took was to define an approach to impact that worked for our investment team and was rooted in our beneficiaries’ non-financial priorities. This was an involved process that brought together stakeholders with different perspectives, but this level of engagement was imperative to deliver an approach that would have longevity.

Broad consultation was key to a credible approach

At this stage, we spoke to several of our peers with impact investing practices, as well as leading industry bodies such as the PRI, the Impact Management Project (IMP) and the Global Impact Investing Network (GIIN). Listening to peers and established industry bodies was instrumental for all actors to have confidence in our approach.

Following this, we came up with a list of six core requirements for our approach:

Formulating these requirements were essential – clarifying and guiding all our further work on impact. Regularly checking back to these requirements ensures our activities remain focused on our original aims and fully in step with the needs of our beneficiaries, stakeholders and the core mission of the Church.

STEP TWO: AGREEING OUR IMPACT PRIORITIES

There are many environmental and social impacts we could look to achieve through our investment activities. To narrow these down, we looked at core principles of the Anglican faith to help identify non-financial outcomes that are most important to our beneficiaries.

Having identified the most critical non-financial outcomes, we translated these to financially tangible impact themes, using the PRI’s Impact Investing Market Map and the GIIN’s IRIS+ system to help identify such themes and ensure that no material impact themes were missing from an investment perspective.

The SDGs offer a clear and common framework to articulate impact

We then mapped these themes to the goals and sub-goals of the UN’s Sustainable Development Goals (SDGs). Although the SDGs were created for the use of governments and policy makers – and therefore are not directly transferrable to the private sector – we felt SDG mapping was important for two reasons: first to help articulate the impact of our investments in accordance with a globally-agreed sustainability framework, and, second, because of the SDGs’ increasing prominence in the investment industry as a common framework and language.

These impact themes are divided across environmental and social issues. For example, one of the Church of England’s stated missions is to ‘safeguard the integrity of creation and sustain and renew the life of the earth’, which we linked to eight investable environmental impact themes – see Figure 2 below. These in turn map to relevant goals, sub-goals and potential measurement indicators of the SDGs, which allows us to see how we are contributing to these goals in a consistent way. We outline this exercise for two of our themes in Appendix 1.

We appreciate that not every investor has guiding ethical principles as clear as a faith-based investor. However, throughout this process we recognised the clear overlap between the Church’s missional goals and the SDGs. As noted, although the SDGs have limitations in a financial context, we believe they offer a comprehensive framework to help identify social and environmental issues, and are extremely helpful in communicating material real-world impact.

STEP THREE: MEASURING OUR REAL-WORLD IMPACT

Having agreed our impact priorities, we then looked at the difficult issue of how to measure the alignment and contribution of our investments to these social and environmental issues. Following our discussions within the market, we found there was growing consensus in using the Investment Management Project’s

five dimensions of impact as an effective approach to conceptualise the real-world impact created by an enterprise.

We felt that the IMP’s explicit distinction between an enterprise’s impact and the investor’s own contribution to impact was important. An investor’s impact on the world comes not just from the impact of their underlying investments, but their own actions (e.g. shareholder engagement and voting) or the actions of their investment managers.

The IMP’s five dimensions of impact offer a way to assess comprehensively an investment’s impact. However, as an asset owner with hundreds of underlying investments, we are unable to assess each company individually using this framework. We therefore explored ways in which we could use the IMP’s approach in a more practical way to identify impact alignment across our portfolio. To see these, please download the full report here, page 11.

STEP FOUR: ASSESSING OUR PORTFOLIO AGAINST THE FRAMEWORK

Having developed a framework, we then assessed how it could be applied to our existing portfolio. Out of necessity, the means of assessing our portfolio against the framework was slightly different across each asset class.

Public Equity

Like most asset owners, the Church Commissioners hold public equity positions in hundreds of companies. This makes it effectively impossible to assess the impactful business activities that every company is involved in. It was therefore necessary to use a third party to help us.

A number of data providers and consultants offer services that offer to identify a public company’s exposure to impact themes and/or the SDGs.Our goal was to find a provider that:

- offered an approach and impact classification that aligned closely with ours

- would therefore enable us to use an automated process rather than a more time-consuming, and potentially expensive, custom service

- covered a large universe of companies and had further plans to develop their service.

Although no single provider offered a perfect solution, several had offerings that provided a lot of the information we wanted. Having chosen a provider, we aligned their own classification to ours as far as possible, allowing us to see revenue alignment across impact themes for the vast majority of our public equity holdings.

Aggregating this information up to the investment fund level allows us to see which of our managers are invested in companies with strong impact alignment. We can compare the level of impact alignment of different managers in our portfolio (within and across asset classes) and against specific market benchmarks. This helps us arrive at a more complete picture of our managers’ commitment to responsible investing; a portfolio with strong

ESG characteristics but very limited impact alignment, for example, may be missing the bigger picture.

As well as assessing impact alignment, we look at the active ownership efforts of our public equity managers. Those with a strong commitment to stewardship and active shareholder engagement are likely to deliver more real-world impact than through capital allocation decisions alone.

Private Markets & Real Assets

There are no off-the-shelf solutions for impact measurement within private markets. Therefore we had to conduct our own manual review of impact alignment for our private assets. For this, we developed the following steps:

- Identify portfolio holdings: We obtained a look-through analysis of the underlying companies or assets held within each fund/manager, including latest fiscal year revenues. This information came from quarterly and annual reports, ESG reports if available, as well as our own internal data systems and analysis from consultants we use.

- Determine impact alignment: We assessed each company/asset based on our framework to determine the percentage of its revenues that align to our impact themes. This assessment was primarily made through reports and information provided by our fund managers, as well as publicly available information such as company websites. As we are given industry verticals and descriptions of the companies we invest into, it was not a particularly arduous task to identify the companies that may align with our impact themes, before going into further depth on potentially applicable companies.

- Calculate our impact contribution: We then pro-rated the proportion of our attributed revenues – or other appropriate measure – to our investment share in each company.

Throughout this process we identified that many companies do report output data both publicly and privately (for example, number of patients treated in a health clinic), but that this was unstructured and with limited application for comparability between companies.

Some companies reported in line with GRI reporting standards. However, we felt that currently this information is of limited use to us – partly because not all companies report across the same disclosures, and also aggregating this information manually for our portfolio companies would take a significant amount of time. If this data was centrally provided, or if our managers provided data on a fund level, then this would be significantly more useful. Generally, however, we felt that the availability of output data was encouraging. It may not be a significant stretch for many private companies – and therefore investment managers – to begin to report non-financial output data and, in turn, understand how financial growth influences potential non-financial outcomes.

Assessing impact across our private equity and real asset holdings has also helped us to identify what additional information we need in order to get a better understanding of parts of our portfolio. One example is the supply chain structure of our forestry assets. Sustainably- certified forestry is often regarded as a sustainable investment. But to be able to articulate its carbon benefit and the associated positive outcomes accurately, an investor needs to know what products the harvested wood is used for. Timber products that displace other materials and are designed for long-term use have much better sustainability characteristics than single-use items. However, the downward supply chain of timber products from suppliers is not generally well known.

Out-of-scope Assets

There were many instances where we were unable to get the information that we required to make an impact assessment. We classified these as ‘out of scope’ in our analysis. Generally, investments that we regarded as out of scope fell into three buckets:

- Investments where the underlying number of companies were too numerous for us to effectively assess, given the amount invested in each. such as in fund-of-fund mandates.

- Where information/data was lacking from our investment managers to make an appropriate assessment at the enterprise level.

- Certain strategies where impact – unless a stated objective of the fund with positive impact coming from the investor’s contribution – is not an immediate effect of investment. An example of this would be derivatives strategies.

Fixed Income

The Church Commissioners’ portfolio currently does not invest in corporate fixed income. Therefore, processes for mapping this asset class to our impact framework have not been required.

To see the full report with Aaron's conclusions, learning and a case study click here or access as a PDF below.

Aaron Pinnock is a member of II Network. To discuss the content of this article and further engage with him, comment below or Sign up today.